Over and Out: Mongolia defies critics and confounds expectations

EXECUTIVE SUMMARY

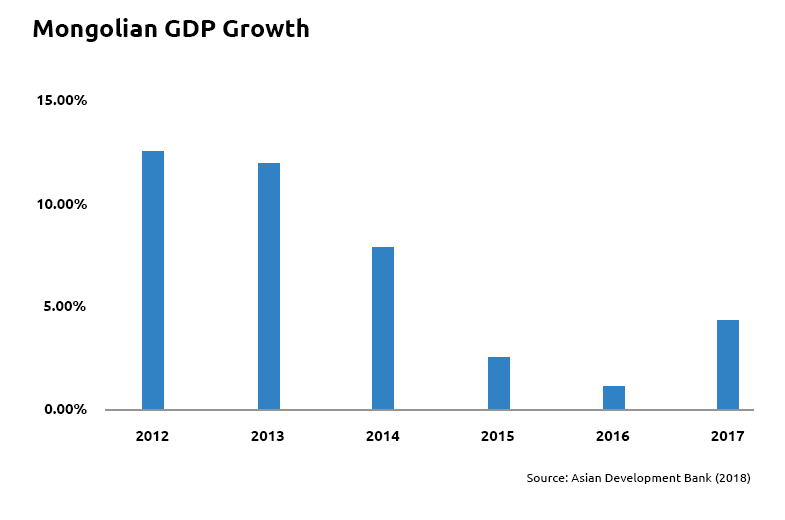

- Upward revision of Gross Domestic Product (GDP) forecasts – Asian Development Bank (ADB) estimate 4% growth in 2017 (ADB)

- Acknowledgement – that in spite of early year uncertainty – Mongolia is ‘rapidly recovering’ (ADB) according to the International Monetary Fund (IMF)

- Rio Tinto announcing estimated doubling of production from Oyu Tolgoi in 2018 (mining.com)

- Industry producing 34% more in 2017 compared with 2016 according to preliminary results (Montsame)

- Coal extraction increasing 136% and sales up 120% (Montsame)

- Foreign exchange reserves reaching a new high in December alongside record results for equities (Xinhua)

Overview

After a rocky start to 2017, Mongolia exceeded expectations. With a chorus of international organizations urging caution, Mongolian policy makers and industrialists rose to the challenge. Trade with China boomed (Xinhua). Exports of key commodities ramped up. And by the close of 2017, the IMF stated growth had been ‘more durable than anticipated’ (Reuters). Alongside upward revisions in growth forecasts from international bodies, Mongolia got its house in order. Budget cuts and structural reforms led to a reduction in the fiscal deficit to 7.5% of GDP (from 17%) (Reuters). As geopolitical uncertainty continues to play on the minds of politicians globally, Mongolia enters 2018 with renewed optimism. Neil Saker, the IMF representative in Ulaanbaatar, once stated his aim that the country would attain 8% sustained growth in line with emerging Asia (MLBF). Just as Mongolia outperformed in 2017, we’re hopeful 2018 will see it grow faster than analysts project.

Minerals & Extractive Industry

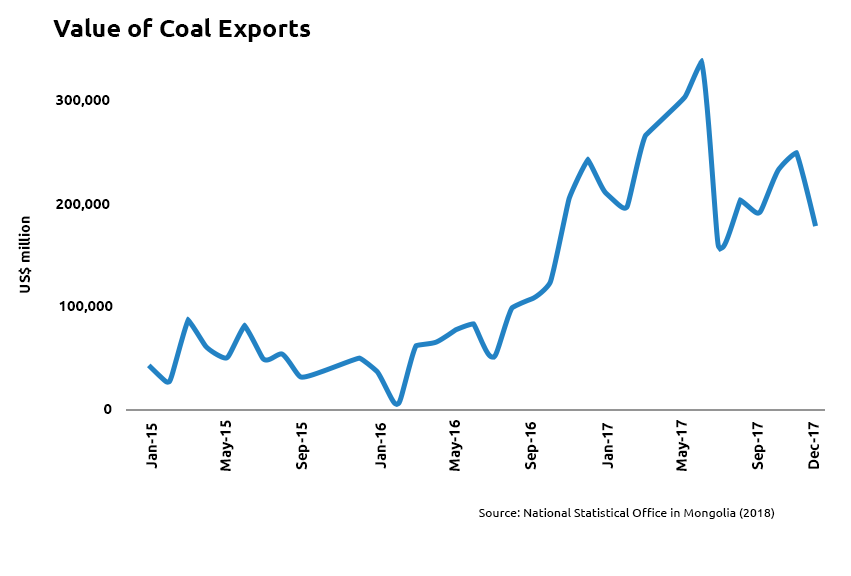

As with early quarters, the final months of 2017 saw a series of announcements from junior and senior miners as to the initiation or acceleration of activities in Mongolia. In late October, Xanadu, announced successful extended drilling on its copper deposits (Proactive Investors). Steppe Gold, meanwhile filed for an initial public offering (IPO), of its common shares (PCJ). In a move which is positive for the underdeveloped but prospective gold sector, Steppe continues its focus on the Altan Tsagaan Ovoo (ATO) project (PCJ). Aspire Mining also successfully completed a US16.5m pro rata renounceable entitlement offer, the proceeds of which will be used to take its Nuurstei coking coal project to production within eighteen months (Proactive Investors). Though individually unlikely to contribute much to the economy in the near term, they show confidence in Mongolia and greater market participation in the mining sector. One of the most eye catching announcements of the last quarter of 2017, was from Turquoise Hill Resources (the majority owner of Oyu Tolgoi). Asides a foreseen 2.8% reduction in operating costs in 2018, it expects to more than double its production of minerals in 2018 (mining.com). This – together with other developments – will help in ensuring that by 2025, Oyu Tolgoi is the third largest copper producing mine in the world (mining.com). With increased electrification and automation, Mongolia is set to benefit from this significant project, that continues to have an outsized impact on the economy. Looking at the overall performance of commodities, coal was the star performer of 2017. The value of Mongolian coal exports was up over 130% compared with 2016, with volumes up 30% (NSO). Figure 2 shows the increase between 2015 and 2017. Even with a reduction in December, it is still nearly quadruple that of early 2015 (NSO). The reasons for this growth are much documented, but principally owe to the closure of hundreds of mines in Inner Mongolia. This has meant Chinese steel producers have looked for alternative sources of coal in order to continue operations. Assuming Mongolia is able to disperse the 40km traffic jam at the border with China, there is reason to anticipate further export growth in 2018.

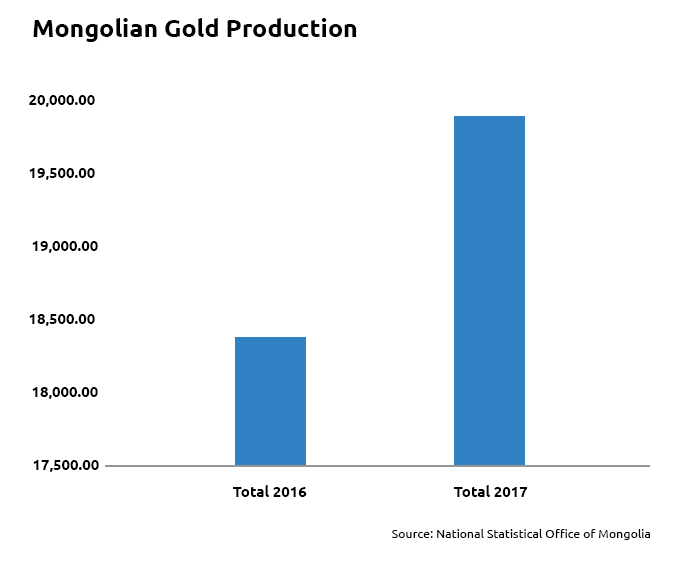

The performance of copper in 2017, flat lined in value terms when compared with 2016. Indeed, there was only a 0.33% increase in the total value of exports (NSO). This reflects a reduction in the overall volume of copper sales, making earlier news as to an expected uptick in the performance of Turquoise Hill assets in 2018, all the more important. As the mine develops and other participants enter the market (not least Codelco), it is hoped a higher caliber of copper will be accessed, powering the sector. We earlier reported that the International Copper Association (ICA) foresees a nine fold increase in global demand by 2027, with Mongolia benefitting given it has the thirteenth largest reserves in the world (ICA). Gold has had a tougher year than earlier estimates suggested. Figure 3, shows overall gold production was up marginally compared with 2016, however, not significantly. The second half of the year represented an improvement but more will need to be done to encourage the development of this sector.

At APIP, we believe that though it is necessary to rebalance the Mongolian economy away from overdependence on commodities, it is also right to acknowledgement that demand drivers differ for its key exports. Mongolia is believed to have as much as US$2.5 trillion of minerals lain under the ground, and until recently, only 10% of the country was available for exploration. The fortunate reality of this situation is that though coal outperformed in 2017, Mongolia’s vast endowment of other finite resources has the potential to insulate if there is downturn in demand for one. The opportunity for Mongolia in 2018, is to ensure that each has the infrastructure and investment to make a meaningful contribution to the economy.

Politics

After the much publicized political machinations of earlier in the year, 2017 seemed poised to end in relative calm. Or so it seemed until early December. President Battulga elected to veto the governmental budget on the grounds it would lead to violation of the agreement with the IMF (Bloomberg). Under the IMF deal, Mongolia undertook to end monetary expansion, together with instituting austerity measures to repair the public finances. Presidential powers in Mongolia are relatively limited, however, Battulga used his veto on the basis the budget deficit would hit 9.5% of GDP under current plans (Bloomberg). Though this may cause stasis, it is encouraging. Battulga was criticized by detractors as an unabashed populist, likely to be confrontational with the IMF. In the event, he has proven himself quite the opposite. His criticism of inefficient investment and construction of new government buildings, points to a leader keen to avoid some of the excesses of past booms. Resolution of issues will be needed, but his willingness to stand up to the legislature in the interests of maintaining the trust of the IMF should cheer investors.

Reform, Consolidation & Market Confidence

In October, the Mongolian government announced a new sovereign bond of some US$650m, with a 5.5 year maturity. In the end, it attracted US$5.5bn of orders for a total issuance of US$800m (Bloomberg). As Bloomberg noted at the time, Mongolia could only attract US$750m of orders for a previous $500m issuance, priced five percentage points higher than that issued in November 2017 (Bloomberg). Though this development is in line with emerging market sovereign debt, it does indicate increased confidence in the country’s creditworthiness. More importantly, recent issuances mean Mongolia has paid down more expensive debt and pushed maturities back. Even though Mongolia is demonstrably recovering, it still needs breathing space to entrench reforms and invest in infrastructure and human capital. This latest run at the markets strengthens the country’s debt position as it moves into 2018. Another example of Mongolia’s improving image is provided by the performance of the Mongolian Stock Exchange (MSE). Though only thinly traded, the MSE continued to outperform in the last quarter of 2017. As Figure 4 demonstrates, the top twenty companies on the MSE increased 63% in 2017, making it the third best performing stock market in the world (gogo Mongolia). In 2017, the MSE traded 859.2 billion Tugrik, the highest in its 26 year history-57.2% ahead of its previous record in 2015,(gogo Mongolia) placing the value of the stock market at its highest level in five years (gogo Mongolia). Given this is one of the easiest means for a foreigner to gain exposure to the country, it is a welcome trend, albeit one in line with the outperformance of equities more generally. We monitor the MSE closely and hope to see new listings in 2018 to demonstrate further market activity.

Confidence owes greatly to the IMF package, however, without structural reform from government, it would likely flatter to deceive. In the summer, commentators described Mongolia’s tax regime as comparable to Middle Eastern countries. Indeed, Mongolia was placed on a black list by the European Union, after equating its system with that of a tax haven. Though overblown, the need to raise taxation to create a more equitable society and economy, has been acknowledged by policy makers. Progressive taxation above the flat rate of 10%, will be introduced, which could bring in 10.7% in additional revenues in 2018 (Montsame). Seven forms of taxation are being phased in, with the principal sums accruing from increases in income tax, social insurance and Value Added Tax (VAT) (Montsame). Increased levies on income are forecast to affect only 5% of Mongolians. Historically, Mongolia, suffered a reputation for fiscal profligacy that left insufficient provision for hard times. This modest move, maintains the country’s competitiveness while allowing greater distribution of the proceeds of growth. In keeping with the government’s attempts to shore up the public finances, it has also stepped up its gold purchase program. As of November, the Bank of Mongolia (BoM) had purchased over eighteen tons of gold – a figure markedly ahead of the previous year (AKI Press). Mongolia’s foreign exchange reserves also reached a new high in December (Xinhua). Totaling US$2.5bn, experts predict this will reach US$3.8bn by the end of 2019, and US$4bn by 2020 (Xinhua). Historically, the country has had an average of US$1.6bn of reserves, with a high of US$4.1bn achieved in 2012 (Xinhua). The steady increase seen this year, is a welcome development designed to increase the resilience of the economic system. The negativity of January 2017 – as heavy, but no less toxic than UB’s winter pollution – has begun to lift. Industrial output in Mongolia was up 30% by year end, and investors are returning (NSOM). This has enabled Mongolia to continue to embed the multilateral program for reform. Japan has announced a US$283m soft loan, as part of the agreement reached by Tokyo and Ulaanbaatar in March (NSOM). This financing will be set at a 0.8% per annum interest rate over twenty years, with a six year grace period (NSOM). If used wisely, this will allow the Mongolian government to finance social, economic and budgetary reform. International support and domestic proactivity have combined to lay a smoother path for 2018. In response to positive economic indicators, the Monetary Policy Council of the BoM announced in December a reduction in interest rates to 11% (NSOM). Bayardavaa Bayarsaikhan, a director of the Monetary Policy Council, predicted 8% inflation in the years 2018-2020, with the rate reduction reflecting the improved economy (Xinhua). All of these factors, prompt a cautiously optimistic assessment as we embark on the New Year.

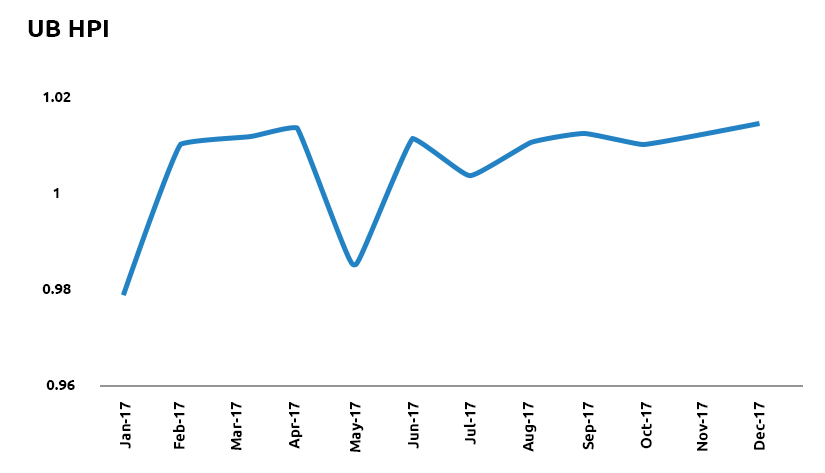

Mongolia’s real estate landscape remains fragmented, especially in the residential sector. APIP’s subsidiary, Mongolian Properties (MP) tracks occupancy in buildings throughout the city. In Sukhbaatar and Khan-Uul, the best buildings suffer few voids, and competition for units is pushing up rental yields at a time when property prices are still low. A mismatch between units commissioned and those actually delivered, means rents continue to rise in prime buildings, but this is not replicated across the city. The Ulaanbaatar general house price index (HPI), shows an increase of 0.34% compared with the same month in the preceding year (Mongol Bank). New house prices are up 0.75% in the same period (Mongol Bank). Older buildings, however, continued to fall by 1.16% over twelve months – trends shown in Figure 5 (Mongol Bank). In 2018, we expect modest improvements in house prices across the board, but prime units in city center locations, to begin to more closely track GDP growth. From a commercial and retail perspective, the situation still remains challenging. Over supply of office buildings in previous years, means occupancy remains comparatively low, albeit, this is likely to change with increased investor activity in the country. Demand for retail space has increased with consumer confidence, however, at the prime end of the market, buyers and tenants remain discerning in their selection of space. The land market meanwhile, heated up at the end of the year in anticipation of potential new holding taxes, especially in central Ulaanbaatar where there remains a shortage of well positioned, unencumbered sites.

Toward a More Balanced Economy

As has been reported in previous bulletins by APIP, the continued support of international organizations is vital to a balanced economy. In late October, the ADB, announced its strategy of support for Mongolia, up to and including 2020 (Aki Press). Amounting to some US$1.2 billion, the ADB’s representative, Yolanda Fernandez Lommen announced support would be based on three key pillars.

- Economic and social stability;

- Infrastructure; and

- Environmental stability.

Broadly unobjectionable from a thematic perspective, we will closely monitor their implementation. Alongside this, there is increasing recognition of the need for substantive reforms to funding of small and medium sized enterprises (SMEs), which could help pluralize the country’s economic base (Aki Press). As in many emerging and frontier markets, access to competitive sources of capital for growth businesses can be challenging. The International Finance Corporation (IFC) – a member of the World Bank (WB) Group – worked with the BoM, to reform Mongolia’s secured transactions system (Aki Press). A key – and useful development – in this regard was the establishment of a pledge notice registry to allow creditors to look for existing charges over assets (Aki Press). By introducing this level of transparency, it is hoped the debt market will function better, allowing it to support the development of Mongolian SMEs. The outcome of the country’s asset quality review, will also help investors understand levels of delinquency and bad debt, and may present investment opportunities. Mongolia, with a land mass the size of western Europe, but a population of scarcely three million, has much untapped potential when it comes to agriculture. Sometimes dismissed as a medium term priority in light of the country’s incredible mineral wealth, it will be an important means of diversification in the future. Just as China has been receptive to increased mineral exports, in December, Beijing indicated its willingness for this also to extend to mutton and beef (Global Times). This development will build upon the impressive fivefold increase in exports of meat products achieved since 2013 (Global Times). In order to build upon this momentum, Mongolia will need to enhance its processing capacity, but it shows the proactivity we have begun to associate with Mongolian policy makers since the IMF deal. 2018 will provide a further opportunity for the Mongolian government to exploit its unique position and potential across sectors.

International Relations

Mongolia’s interaction with China continues to grow – as relations between Beijing and Ulaanbaatar warm. In October, both sides, announced acceleration of ongoing projects including soft loan and non-refundable aid on construction of paved roads and bridges (Montsame). But it is not only with major trading partners, that there is a drive for greater diplomatic and economic interaction. Mongolia has signed an agreement on cooperation with Slovakia. Signed at the end of November, the agreement paves the way for the broadening of cooperation in areas of food, agriculture, information technology, mining and education (AKI Press). More tangible, perhaps, are reports that there has been progress in the much discussed finance for a oil refinery in Sainshand with Indian assistance (Energy Infrapost). Mongolia produces around eight million barrels of crude oil per annum, however, it has limited refinement capacity and relies on imports from its neighbors (Energy Infrapost). According to Sputnik, a US$700m loan has now been approved, alongside a further US$264m for oil pipelines (Energy Infrapost). Mongolia’s Ambassador to India, G Ganbold is quoted as stressing the important role this will play in reducing energy independence and in delivering foreign exchange (Energy Infrapost). Mongolia’s location requires careful diplomacy, however, 2017 (especially since the election of President Battulga), has seen an increasingly self-confident Mongolia, engage with the world.

Conclusions

2017 has come and gone, and Mongolia-observers cannot help but feel a little easier than one year ago. The IMF, the ADB, pundits, commentators and policy makers, all revised their estimations of growth upward as the year progressed. Mongolia is not at the dizzying heights of 2011, but it’s also a long way from the nadir of 2016. It’s repaired relations with China, unleashing a boom in activity, all the while boasting a 30% increase in industrial output (NSO). From Xanadu to Steppe, Rio to Kincora, momentum is returning, with weekly announcements of progress, especially in the extractive industry. Oyu Tolgoi, the posterchild for Mongolia’s growth, is due to double production in 2018, facilitating the next chapter of Mongolian development. And, though vital, it is supported, by many more industries beside. But growth, without prudence, can lay the basis for economic calamity. This time, people are beginning to dare believe that things have changed. The government has upped gold purchases and stock piled foreign reserves. The President has vetoed a fairly modest budget, because it could worsen the deficit. The IMF package is fully on track, and an asset quality review underway. And the markets seem to recognize this maturity. Mongolian sovereign debt is oversubscribed and trading keenly, the stock market is at record highs, and superpowers like China and India, as much as smaller partners like Slovakia and Belarus, are talking to the government and offering support. As Mongolia moves into 2018, and as the snow thaws, both literally and figuratively, there is no room for complacency. But Mongolia with its admirable achievements in 2017, has a fighting chance of reopening for business and priming its economy.

For help navigating opportunities in Mongolia, please contact Andrew McGregor (andrew@apipcorp.com) or Lee Cashell (cashell@apipcorp.com).